“The hardest thing in the world to understand is the income tax.” ” -Albert Einstein

If you’ are a high-income enterprise technology sales professional, you have probably noticed something unsettling: The more you earn, the more complicated—and punishing—your taxes become.

Between W-2 income, commissions, bonus’s, vested RSUs, and stock options, you may be making $400K, $700K, even seven figures—and yet still feel like you’re leaking money to the IRS every quarter.

You’re not imagining it. And you’re not alone. I was in the same position.

Let’s break down why this happens—and how many Technology Sales Leaders are using real estate to legally and strategically change the game.

1. You’re Earning More—but Keeping Less

Let’s say you’re making $350K in base salary and $200 in vested RSUs and $100 Commission/Bonus ($650k Total).

At first glance, that’s fantastic. You are exceeding expectations, hitting all of your targets. But when you layer in:

- Federal income tax rates (up to 35-37%)

- Federal Supplemental income tax (commissions & bonus) 22% since it’s under $1M

- Federal RSU Grants Tax is 22% of the market value at time of vesting

- State income tax (up to 13.3% in California where I live)

- State bonus and vested RSU tax rate is 10.23%

- State Commissions are taxed at 6.6%

Let’s not forget all the other little taxes like mediate and social security.

Suddenly, you’re paying $200K+ in taxes every year—without even realizing it. 40% to 45% of your earnings are lost to taxes depending on your marital status and other deductions…which are minimal.

Your commissions and bonuses? Taxed at the highest bracket. Your RSUs? Taxed the moment they vest. Your deductions? Minimal compared to your income.

You are playing a high-stakes game with no shield—unless you change the rules.

2. The Problem with W-2 Income (Salary/Bonuses/Commissions/RSU’s)

W-2 income, or active income, is the most heavily taxed income class and withheld from your monthly earnings by your employer.

You can not deduct much. You can not defer much. And you are taxed at the top marginal rate with every new dollar earned.

Bonus and Commissions: Wonderful incentives but taxed heavily.

RSUs (restricted stock units) are wonderful incentives but are the worst from a tax perspective: they are taxed as ordinary income at vesting, not when you sell. This is taken out of your paycheck at vesting reducing your net income that month. If your stock decreases in value after vesting, you have already paid taxes on the higher price value.

What is worse is the resulting tax withholding windfall. This windfall are the additional taxes owned at the end of the year as a result of the “gap” between what the employer withholds and what is actually due.

Result? You are exposed. You are left hoping for long-term appreciation—while taxes eat your earnings today.

3. Why High-Income Sales Professionals Are Turning to Real Estate

Real estate isn’t just about cash flow and appreciation—it is about tax efficiency.

When you invest passively in a real estate or a private equity fund, you gain access to two of the most powerful tax tools the IRS has designed to incentivize investment into housing to address the shortage.

Depreciation-Deprecation is a “paper” loss deduction that is used to offset passive income from the property-even if you never swing a hammer. Because private real estate is a business, it benefits from several deductions including depreciation. This allows you to grow your income without increasing your tax bracket or taxable income.

The 1031 Exchange-The most powerful tool used by the largest investors is the 1031 exchange. They defer any capital gains or depreciation recapture from real estate if you roll the equity distributions from a sale/exit into another property.

For investors, this means depreciation to offset taxes you would normally pay on your passive cash gains AND keeping 20-30% more of your equity gains if you leverage the 1031 exchange.

Now here is the kicker-In many cases, the deprecation can be used to offset taxes on your active W-2 income as well, resulting in large tax refund checks at the end of the year instead of a tax withholding windfall.

THIS IS HUGE!

Imagine doubling your income and net worth without paying any taxes or increasing your taxable income or tax bracket by simply investing in Real Estate that you don’t have to actively manage. Then using the tax benefits to reduce your W-2 tax liability at the end of the year.

As a result, many successful technology sales leaders liquidate their RSUs at vesting when it is at its highest value and invest into real estate for stable income, tax efficiency, and equity growth.

Real-World Example: The Sales Director who Received a $25K Tax Refund

Anthony is a Cramlet Capital investor who is a Regional Director of Sales at a major SaaS firm. He earned just under $400K last year. Roughly $200K was his base salary, another $100k in commissions, and another $100k in RSUs vested. Nearly $200k was withheld from his earnings over the course of that year.

He sold his vested RSU’s and re-allocated $100k into a private real estate opportunity. This reduced his concentration risk and diversified his portfolio with an uncorrelated investment. We provided him with a schedule K-1 that provided $50,000 in depreciation paper loss. His CPA applied the $50,000 in passive depreciation while preparing his tax filing.

End result?

- His investment was projected to yield $15,000 (roughly 5% annually) in cash distributions over the 3 year hold period. This is his passive income. His CPA applied $5,000 in depreciation in the first year and reserved another $10,000 in deprecation to offset future cash distributions (carry forward the depreciation).

- He had a $10k tax shortfall from his RSUs that vested. His CPA then applied the remaining $35k in depreciation to offset the taxes withheld from his W-2 earnings in that first year. This resulted in a $25k tax refund instead of a t$10k tax bill. Please note, he met certain eligibility requirements defined by the IRS including filing jointly with his wife, however many of our investors find themselves in this exact situation. We call this the Golden Ticket.

$25 is a car. Or a full year of tuition.

Or capital to invest into another opportunity and earn more depreciation to use against his active income and get another tax refund the following year.

This was in addition to the $15,000 in annual cash distributions he was receiving; all without increasing his taxable income.

That is the power of depreciation.

Result 2?

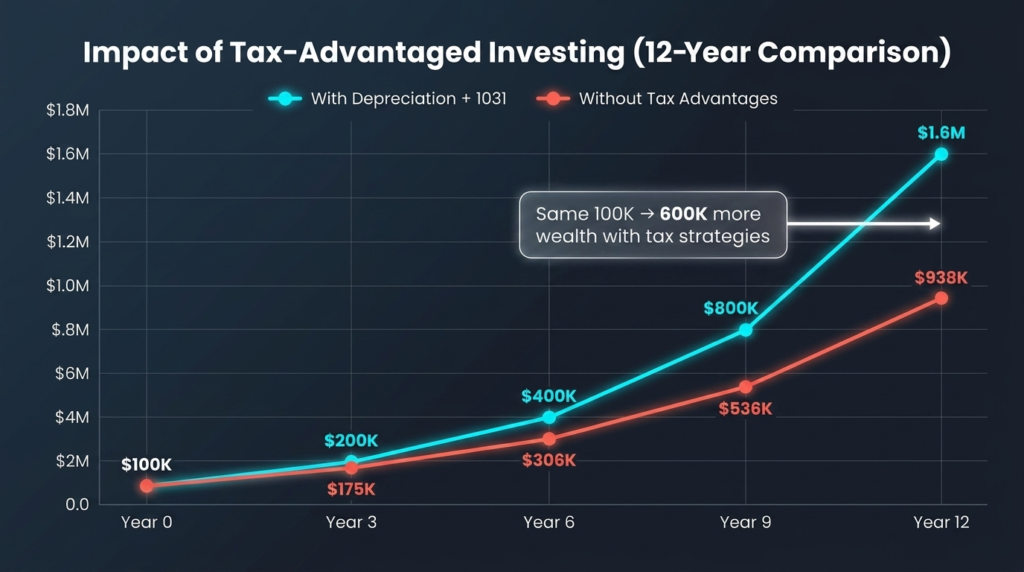

When we exited the investment, he leveraged a 1031 exchange to reinvest in another passive real estate opportunity with us. He kept the $50k in passive losses (no depreciation recapture) and his equity doubled to $200k ($100k initial investment + $100k in gains).

Instead of paying taxes on the gains or depreciation recapture, he was able to reinvest 20% more into the next property. That means 20% more in cash distributions and 20% more in equity growth in the next investment.

The compound effect of this is massive. Over a 12-year period, that $100k could turn to $1.6M leveraging the power of Depreciation and the 1031 Exchange. $600,000 more wealth than without leveraging this tax strategy.

4. This Isn’t a Loophole—It’s the System

These aren’t “tricks.” This is exactly how the tax code is written.

The IRS encourages investment in housing, infrastructure, and real assets by offering these tax incentives to investors. But here’s the thing:

You don’t get these benefits by investing in mutual funds.

You don’t get them with REITs or ETFs.

You only get them by investing directly or passively in private real estate deals that pass through the depreciation to you.

5. Conclusion: Replace Tax Frustration with Tax Strategy and Diversification.

If you’re tired of handing over 40%to 50% of your income to the IRS with little control and want predictable income beyond your earned income, Real Estate may be a great option for you. This isn’t about beating the “system”. It’s about playing a better game—one built on cash flow, equity, and efficient taxation.

Diversifying your net-worth and investment portfolio by re-allocating a portion of your RSU’s or commissions is an intelligent play. Most Sales Leaders are heavily concentrated in company stock (W2 Income + Stock Equity) which creates exposure to volatility. Additionally, their incentive pay and high compensation becomes a real tax drag and liability that passive real estate investments can address directly and indirectly.

Real estate offers:

- Consistent passive income without increasing taxable income.

- Considerable Equity Growth

- Tax Advantages not found in public or active investments

- Ability to offset active income

- Stability outside of the tech sector

It’s not about quitting your job or going all-in—it’s about adding one asset class that starts working in your favor.

6. Next Steps

Whether you are a seasoned or new investor, adding institutional grade real estate to your portfolio can provide a strategic advantage to your short term income growth, long term wealth goals, and provide strong tax advantages . We invite you to schedule a call to understand if your investment goals align with our investment thesis and if you qualify for the Golden Ticket. We look forward to speaking with you.