What is a Capital Stack in Real Estate?

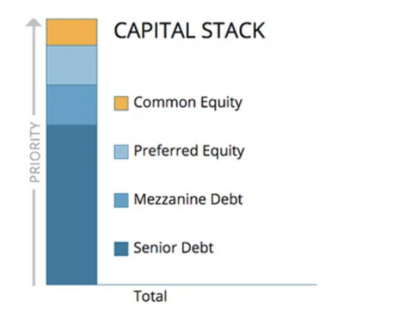

The “Capital Stack” in a real estate transaction is the collection of capital used to finance the purchase of the property. Depending on the complexity of the transaction, there can be several layers to a Capital Stack however we will keep our analysis to the four most commonly used types of Capital in ascending order of priority and increasing level of risk: Senior Debt, Mezzanine Debt, Preferred Equity, and Common Equity.

Senior Debt

An easy way to think of Senior debt is as a loan from a bank or real estate specific lender and it sits at the top of the capital stack. The amount of senior debt varies by transaction, but typically makes up 60% – 80% of the purchase price. So, for example, a property with a price of $1MM could have senior debt of $600,000 to $800,000. In return for their loan, the senior lender’s position is secured by a first position lien on the property itself. This means that they are first in line to receive any money produced by it (for their loan payments) and have the ability to initiate foreclosure proceedings if the borrower does not meet their obligations under the loan agreement. The senior debt holder is generally considered to be the least risky position in the capital stack and earns the lowest interest rate as a result.

Mezzanine Debt

On occasion, there is a gap between the amount of debt that the senior lender is willing to provide and the amount of money that can be raised from equity investors. In such cases, this gap is filled by Mezzanine Debt which is also secured by a lien on the property, but it is subordinate to the senior debt holder. This means that they are second in line to receive money produced by the property, which puts mezzanine lenders in a slightly riskier position than senior debt holders. As a result, the interest rate charged for mezzanine debt is higher.

Preferred Equity

In most commercial real estate transactions, a single purpose entity is formed as the purchasing vehicle for the investment property. Where senior and mezzanine debt is secured by an interest in the property itself, Preferred Equity is secured by an interest in the property’s ownership entity. Preferred Equity investments entitle the holder to receive a “preferred return,” meaning that preferred equity holders are first in line to receive a share of whatever cash flow is left after all debt payments have been made. Because preferred equity investors do not have an interest in the property, their position is considered to have higher risk than debt holders. They are third in line to be repaid.

Common Equity

Finally, Common Equity holders are individuals who also purchase shares in the property’s ownership entity, but their interest is subordinate to preferred equity investors. This means that they are last in line to receive money produced by the underlying property, making their position the riskiest of the four. But, in return for the additional risk, common equity investors also have a chance to participate in the profit produced if the property is sold for more than the purchase price. As a result, they have a chance to earn a higher return than other members of the capital stack.

While there are four components of the capital stack, the reality is that many commercial real estate transactions, including ours, are financed with a combination of senior debt and common equity. Mezzanine debt and preferred equity raise the overall risk profile of a transaction and complicate administration of the investment, which make them options of last resort. To illustrate why it is important to understand the composition of the capital stack, an example is helpful.

Why the Composition of the Capital Stack Matters: An Example

Assume that a commercial real estate (CRE) firm has identified a multifamily property that represents an excellent investment opportunity. They place it under contract for $1,000,000 and, after a period of due diligence, decide to proceed with the transaction. To finance the purchase, they obtain a commitment for a bank loan of $750,000 and sell shares in the purchasing entity to raise the remaining $250,000. In this scenario, the bank loan represents the senior debt and the investors who purchased shares in the ownership entity represent common equity holders. This means that the rental income produced by the underlying property is used in the following order: pay the property’s operating expenses, pay the property’s loan payments, distribute excess capital to equity investors.

For two years, everything has been fine. Tenants are paying rent and the property is full. However, an economic recession strikes, and a high percentage of the property’s tenants can no longer make their rent payments. As a result, there is not enough income to make the property’s loan payments and the borrower defaults. To protect their investment, the senior lender moves to foreclose on the property and take possession of it. Because they are not in the real estate business, the lender immediately puts the property up for sale, but because of current economic conditions, they are only able to sell it for $800,000. This is where the rights and priority order of the capital stack are critical.

Assume that, at the time of foreclosure, the senior loan has a balance of $750,000. Because the senior lender is first in line to receive funds, they are entitled to $750,000 of the sale proceeds, which they will use to satisfy the loan’s outstanding balance, so they are paid in full. The remaining $50,000 will go to common equity holders and it is very clearly less than their $250,000 original investment, which means that they will only receive a fraction of their initial investment back.

While this scenario may make it seem like common equity investments are scary, it is important to consider the flip side of this scenario as well. Assume the same situation, but everything with the property goes well. For 5 years the property operates as planned, rents go up, and it is ultimately sold for $1,250,000 while the loan has an outstanding balance of $600,000 at that time. In this case, the sale proceeds would go to pay off the loan balance and the remaining $650,000 goes to common equity holders, earning them a profit of 2.6x their original investment.

The point is this, real estate investing involves risk and there is a distinct relationship between the amount of risk that an investor takes on and the potential return that they can realize. For this reason, it is critical that each investor understand where their investment lies in the capital stack and the rights and repayment priorities that come along with it.

Capital Investment Balances Risk and Reward

Investors commit capital (typically, but not always, cash money) to an enterprise in return for a bundle of rights entitling them to reap financial fruits (or “proceeds”) of the business. Most businesses get their capital from two broad types of investors: equity and debt. Generally speaking, equity capital is more at risk than debt capital because equity holders usually have no absolute right to repayment of their investment principal. Consequently, equity investors enjoy a greater potential upside (through the profits of the business and appreciation of their ownership interests) than debt investors (who receive, at the most basic level, repayment of principal plus a rate of return). Within each broad category of investors, many sub-categories can also exist, such as preferred and common equity, and senior and junior debt. Even these sub-categories can break further into sub-sub-categories, according to a multitude of distinctions among them (e.g., secured/unsecured debt, limited/general partners, conversion rights, and so on).

Conclusion:

Know the Stack, Maximize Your Success

Understanding the capital stack is essential to balancing risk and reward in multifamily real estate investing. Each layer, from senior debt to common equity, offers unique opportunities and risks.

By knowing your position in the stack, you can align your strategy with your goals, invest confidently, and make informed decisions. Real estate success isn’t about avoiding risk—it’s about managing it wisely.

Next Steps: Protecting and Growing Wealth Together

Whether you’re a seasoned investor or new to investing, Cramlet Capital is here to help you protect and grow your wealth through safe, simple, and successful strategies. Let’s work together to achieve your financial goals.